Millions of Americans are Overpaying for Car Insurance — This Website Helps Them Find Cheaper Rates

By Daniel Harper | Reviewed by Laura Mitchell

Car insurance is one of those bills some people don’t question.

You pick a company, set up automatic payments, and forget about it.

But here’s the surprising part: the same driver can be quoted completely different prices depending on the insurance company.

Sometimes the difference is small. Other times, it can be hundreds — even thousands — of dollars a year.

That’s why thousands of drivers everyday are turning to RatesCompare.com, a website that lets people quickly check car insurance rates from multiple companies in one place.

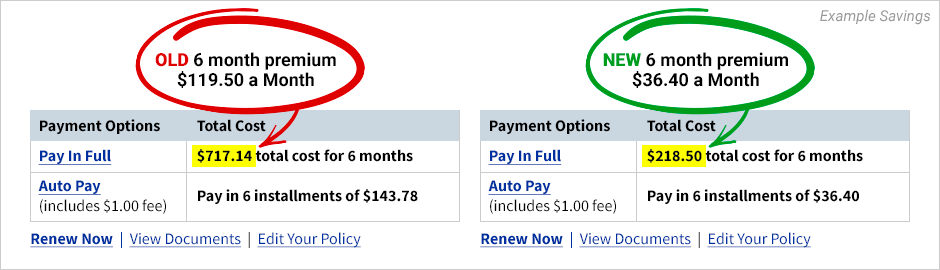

For many drivers, the results can be eye-opening. Survey data shows some drivers save over $1,000+ per year — just by checking.

Why insurance prices can vary so much

Car insurance companies don’t all calculate risk the same way.

Each insurer uses its own pricing model that looks at things like:

• Driving record

• Age and ZIP code

• Type of car

• Credit-based insurance score

• Mileage

• Past claims

Because every company weighs these factors differently, one insurer may see a driver as low-risk while another charges a much higher premium.

That’s why experts often recommend shopping around before renewing your policy.

The simple way drivers are comparing rates

Comparing insurance used to mean visiting several company websites or calling agents one by one.

Sites like RatesCompare.com simplify that process.

Drivers can enter their information once and quickly see which insurers may offer better rates.

The process typically takes only a few minutes.

Some drivers find their current insurer is still competitive. Others discover companies willing to offer lower prices for similar coverage.

Why many drivers never check

Even though the potential savings can be significant, most drivers rarely compare insurance rates.

There are a few reasons:

• People assume the process takes too long

• Many stay loyal to the same insurer for years

• Insurance pricing can feel confusing

But because insurers constantly update their pricing models, rates can change more often than drivers realize.

The bottom line

Car insurance is a major yearly expense for millions of Americans.

But unlike many bills, the price isn’t fixed.

That’s why many drivers are now spending a few minutes online before renewing their policy — just to see what other companies might charge.

And for some, a quick check on RatesCompare.com is all it takes to find out they could be paying a whole lot less for the same coverage.

")

")